On Wednesday, Aug. 24, President Joe Biden announced his promised student loan forgiveness plan for college students, which is called the Student Loan Debt Relief Plan. Government estimates assume that roughly 8 million students are already eligible because the Department of Education already has their income information, and each student is able to receive up to $10,000.

Teresa Rhyne, director of Financial Aid for VWU, explained that the relief plan is meant “for any Federal Direct Loan that was disbursed to a student prior to July 1, 2022,” meaning that loans for “the current academic year will not be part of the Student Loan Debt Relief Plan.”

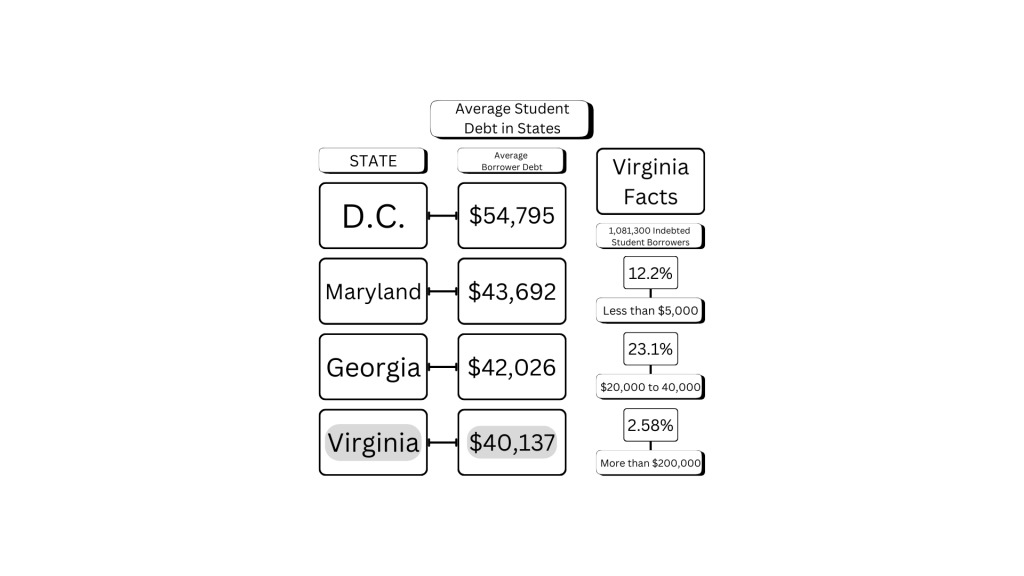

The disbursement of money is as complicated as the disbursement of federal loans. Money is limited to students with an income of less than $125,000 or dependents with a household income of less than $250,000, and students eligible for a Pell Grant at any time of their college career may get an additional $10,000. According to The Virginian-Pilot, about 60% of borrowers of federal loans are recipients of Pell Grants.

The Committee for a Responsible Federal Budget estimates that the plan will cost between $400 and $600 billion, with the ability to assist about 43 million people with student debt.

Rhyne states that this “plan is one-time only,” and encourages students to search for debt forgiveness through the Public Service Loan Forgiveness (PSLF). In addition, she recommends that students check the studentaid.gov website to manage their loans and watch for the release of the application, coming in October.

Even with the services being provided to lower debt, there is still doubt about the effectiveness of the plan long-term. “This may seem like a bleak outlook, but I see this as a bandaid on a bullet wound,” said Political Science student Ryan Christie.

Christie sees the forgiveness plan as “a short term appeasement that does not address the true problem, which is the extremely high cost of higher education.”

Biden has already eliminated almost $32 billion from the $1.6 trillion of outstanding student debt in America through previous plans, but according to Christie, there is still the problem in that the “whole education system has ballooned to costing a small fortune.”

Much of the rise of the cost of college is because of inflation and a lack of economic security, as well as the downturn in enrolled students since the COVID-19 pandemic and the higher salaries for faculty and staff, NBC News said.

Therefore, this plan will be helpful to the “lower-income students,” but this was before the cost will be “transferred to society as a whole,” Christie said.

Criofan Shaw, a senior at VWU, believes that the loan forgiveness plan will have “a positive effect on the debt of most borrowers.” Shaw would also like to see the federal government taking more initiative. “I think Biden is doing the bare minimum in order to boost centrist Democrats in the upcoming election,” Shaw said.

Shaw believes that the federal government has an “innate responsibility” to help eliminate college debt. “If we can continue to send tens of billions to Ukraine,” said Shaw, “we can wipe out federal loan debt.”

For the 2022-23 school year, VWU has frozen the cost of tuition. However, when looking at trends across the country, the rise in tuition is more clear. According to educationdata.org, college tuition inflation averaged 4.63% annually from 2010 to 2020. Additionally, after adjusting for currency inflation, the cost of college tuition has risen by 747.8% since 1963.

The fact sheets published by VWU are available at the institution’s website, beginning with the year 2003. In 2003, the undergraduate tuition was listed at $19,200. By 2021, the tuition had risen by 87.55%, totaling $36,010. When considering currency inflation, the change seems less drastic. Today, that $19,200 is comparable to about $30,915.

Consequences of the loan forgiveness plan will be seen in the coming months, as will possible changes or additions to federal loan forgiveness plans. “Those who had to take out private loans to assist with tuition on top of federal loans (like myself),” Shaw said, “will still be in a pickle, but that does not mean I cannot be happy for others or recognize that I will still benefit from this forgiveness plan.”

By Rhian Tramontana

rjtramontana@vwu.edu